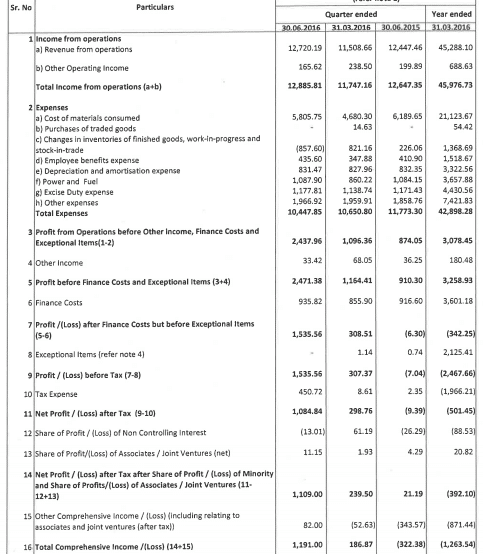

JSW Steel has set a strong benchmark for the steel industry with its astounding Q1 results for the current year. From almost negligible profits from last year to 1084 Crs profit for the current year, the company has come a long way.

The company’s revenue increased by 1.89%, but the profits increased by 50 times.The company’s turnaround story lies with its increase in its operating margin by almost three fold.

- Increased operating margin from 6.91% in Q1FY16 to 18.91% for Q1 current year.

- The operating margin mainly increased due to cheaper raw materials and governments initiative like anti dumping duty, duty on imported steel products, and minimum import price.

- Their finance costs have grown by 9.33% compared to Q4FY16, and 2.09% compared to Q1FY16. Outstanding long term debt as of 31 March 2016 was Rs 32793.22 Crs.

- Currently the company is paying 7.26% of its revenue as finance costs, which is quite high.

Check out the Daily Results Tracker here

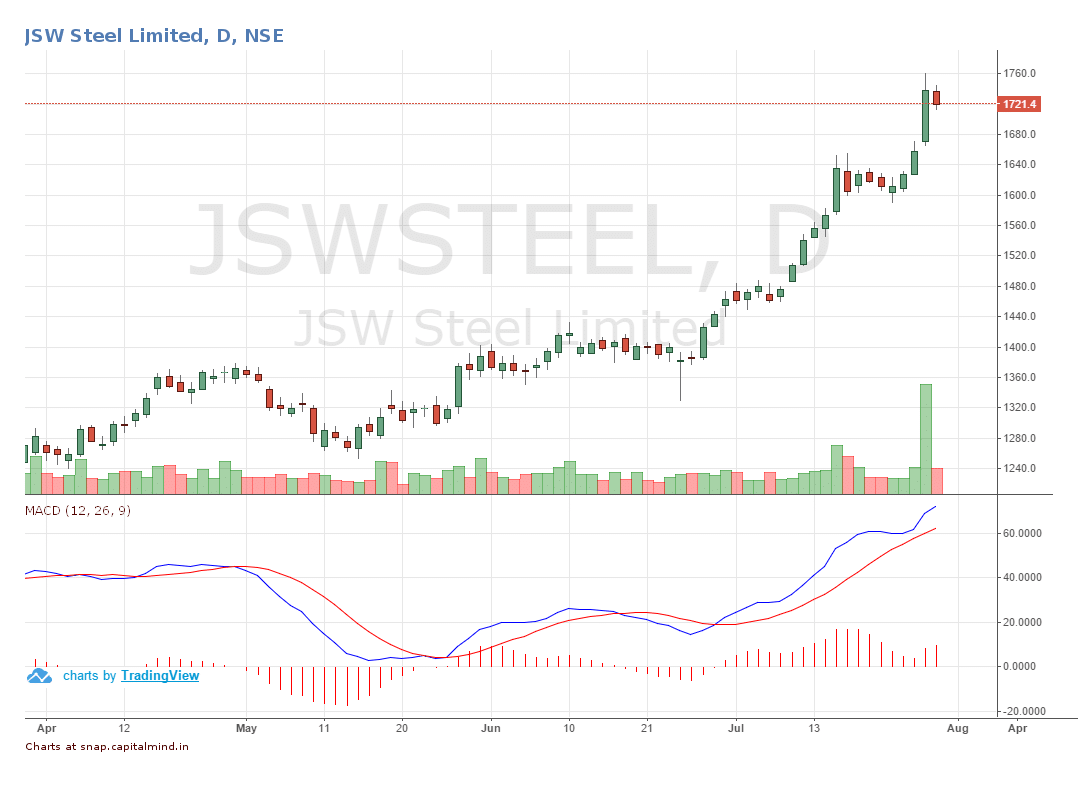

The stock has moved 4% in a single trading session on results day.

While JSW seems to be the most efficient player today, it’s because of the higher minimum import price that it’s able to generate these profits. When the support goes, the companies will go back into extremely low margins. JSW has been an outperformer though, and might be the last to be hit.

Developments and Future Outlook:

- Has increased its blast furnace capacity from 14.3 MTPA to 18 MTPA in Q1 FY17.

- The company has stated the european market is volatile due to the Brexit event, but US has been more stable.

- The company has admitted the domestic demand has been sluggish for the quarter, with only 0.4% growth in consumption but 4.8% increase in production YoY.

- The import of steel have fallen by 30%, post minimum import price implementation against expected drop of 50%. This leaves more room for the government to take some action.

- Cheap exports from China, Korea and Japan are still a risk for the global steel industry growth, however the prices of steel are comparatively more stable due to pick up in infrastructure segment.

You might also like:

- Airtel Profits Drop 31% On Accounting Change, Data ARPU Up To 202: Result Analysis

- Construction and Railway business lead the charge, Escorts reports 33% growth in Net Profits : Results Analysis

- Yes Bank grows profit 33%: Result Analysis

- Optionalysis: Making Money When Markets Fall

- Delivery Shockers – 01/03: Thomas Cook, Future Lifestyle and Speciality Restaurants Show up in Today’s Shockers

![]()

Disclaimer

Nothing in this newsletter is financial advice and should not be construed as such. Please do not take trading decisions based solely on the matter above; if you do, it is entirely at your own risk without any liability to Capital Mind. This is educational or informational matter only, and is provided as an opinion.

Disclosure: The authors at Capital Mind have positions in the market and some of them may support or contradict the material given above, or may involve a direction derived from independent analysis.