Syndicate Bank has come out with its Q1 results. Their net profit took a beating due to NPA provisioning, indicating a rough road ahead.

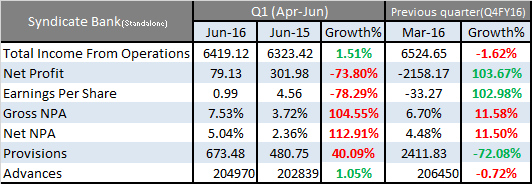

Net revenues increased marginally by 1.51% YoY, but net profit plunged by 73.80%.

heck out the Daily Results Tracker here

Other major analysis points are:

- Operating margin decreased from 17.85% in Q1FY16 to 12.22% in Q1 current year. This was mainly due to operating expense increasing by nearly 43% YoY. Employee cost and other expenses rose by 50% and 30% respectively.

- The provisions have increased by 40% YoY, but the good thing is if we consider QoQ it has decreased by 72.08%. Meaning, most of the NPA’s have now been provisioned.

- Though the advances contracted by 0.72% QoQ, but the gross NPA and net NPA increased by 11.5% each QoQ.

- For Q1 FY16 28.20% of PBT was paid as tax, but for the same quarter last year 45.95% of PBT was paid as tax. This is likely an anomaly last year.

- The share holding percentage of Govt of India increased from 65.17% last quarter to 69.32%. (This is on account of the bailout given to public sector banks in the quarter)

- The only good thing happening over here is writing back of the provisions amounting to 68.82 Crs.

- Syndicate bank has gone a step ahead and has started to make a 2% extra provision on sub standard assets.

Stock prices didn’t react much to the results, and closed 1.3% up.

You might also like:

- Bajaj Auto reports 13.6% Profit Growth despite a 2% dip in sales : Result Analysis

- Yes Bank Grows Profits 33%: Result Analysis

- JSW Steel Reports Outstanding Profits for Q1FY17: Result Analysis.

- Airtel Profits Drop 31% On Accounting Change, Data ARPU Up To 202: Result Analysis

- Optionalysis: Making Money When Markets Fall

- Delivery Shockers – 01/03: Thomas Cook, Future Lifestyle and Speciality Restaurants Show up in Today’s Shockers

![]()

Disclaimer

Nothing in this newsletter is financial advice and should not be construed as such. Please do not take trading decisions based solely on the matter above; if you do, it is entirely at your own risk without any liability to Capital Mind. This is educational or informational matter only, and is provided as an opinion.

Disclosure: The authors at Capital Mind have positions in the market and some of them may support or contradict the material given above, or may involve a direction derived from independent analysis.