This is an archived mail for Capital Mind Premium subscribers, sent on Feb 6, 2014. (Read more)

There’s been some interesting macro-data in the last few days, which seems to have gone largely unnoticed. At Capital Mind, we like to look at data but understand that by-and-large it’s only the outliers that are actionable. That means I could give you a very large amount of data to analyze but in the end, what is actually interesting is:

- Is there something that’s out of the ordinary? Something that’s much lower than it ever has been, or much higher? (Outliers)

- Is there a way to take those outliers and build an investment thesis around them? Can those be tested back? (Actionability)

Different things are actionable for different people, but it’s always a little jigsaw puzzle you have to put together so that you see what’s really happening inside. Let’s take a look at the outlier in government debt – the big repayment – and how it impacts the longer term bonds.

[level-capmind-pro]

An Auction Ditched

In January, one of the government bond auctions of Rs. 15,000 cr. was deferred. This has now been cancelled, since the government has cash flow elements of:

- A substantial dividend from Coal India (18,000 cr.),

- A stake sale of some of the government’s equity in Indian Oil to other government companies (ONGC and OIL) who will pay Rs. 4,500 to Rs. 5,000 cr.

- A follow-on offer to EIL which should get them Rs. 500 cr.

- The 2-G auction process, which shows they’ll get about Rs. 40,000 cr.

This sums up to about Rs. 63,000 cr. which should satisfy the government for now, and it needs only one more issuance, of Rs. 10,000 cr. this week, for the financial year 2013-14.

Note that the government will pay out Rs. 20,000 cr. in debt repayments coming due in February.

Impact: That’s 15,000 cr. debt that’s not been borrowed. Good for bonds, somewhat. But read on.

Debt Switch Happens, But Impact Still Heavy

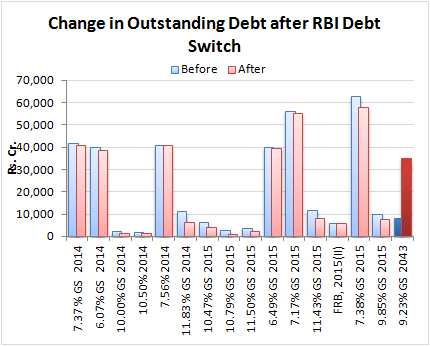

We’ve also noted that more than 89,000 cr. of debt is coming due in April and May. To avoid the massive exposure – these would be the largest debt repayment months in a very long time – the RBI had decided to swap debt that would mature now for debt due later.

This was given a Rs. 50,000 cr. budget and the RBI has managed to roll Rs. 27,000 cr. of it to a longer term, in an announcement yesterday. But which debt? If we look at data on Jan 27 and then on Feb 3, we can see the differences and see where the debt was moved.

The impact is still huge for April and May, which, together, account for Rs. 85,000 cr. of debt repayment AFTER this debt switch.

The debt was moved out to 2043, all of the Rs. 27,000 cr. And it looks like someone got paid Rs. 400 cr. for the switch.

As you can see, the switch doesn’t change the repayment concentration in any substantial way.

Even if the RBI switched the rest of the allocation (Rs. 23,000 cr.) in the April+May months, we would see fairly high redemptions of 62,000 cr. in those months.

Impact: Long Bond Pressure, Specifically the 2023 November bond

What do the above two pieces mean? They give you the outlier: the high repayment. The government doesn’t have this money. It will have to borrow to repay, and it will borrow through long term bonds. Issuance of these bonds will go up.

There will also be a new 10-year bond, which will mature in 2014, issued after April.

The twin pressures of a higher issuance (due to the repayments) and going off-the-run of the current 10 year (the 8.83% Nov 2023 bond) to the new one will cause a serious drop in the price of the current 10 year bond (and higher yield).

We can see that happening even now – the earlier 10 year benchmark (the 7.16% May 2023) was switched to the 8.83% Nov 2023 bond, and while the latter trades today at 8.70% while the former is at 9.1% (you don’t pay that kind of difference for six months!).

The trade idea therefore has to be that the 8.83% bond will see lower prices (and higher yields). We expect that prices will remain under pressure. In our view, a short trade can be entered after the inflation numbers are out in the middle of the month. Inflation is likely to be lower, so yields will fall on the hope that on April 1, RBI will cut rates (which we don’t believe is likely).

There is now an instrument you can use to make trade this – the 8.83% bond on the NSE Bond Futures segment. Liquidity, however, is low, and we might only want to enter the April or May futures (the May futures aren’t available till after Feb 26).

Building A Fixed Income Portfolio

If you don’t really want to trade this but need to understand how it impacts you, it’s going to mean that your fixed income investments in longer term bonds will lose money. Bond funds that have a high “duration” – a parameter which intends to indicate how much time is left for their bond holdings to mature – will be hurt if they hold the 8.83% bond (and most do just for the liquidity).

We would avoid fixed income products that have a long duration, and work closely only with those that are very short term in nature, until there is more clarity on the above repayment, the political situation and of the exit of FIIs from the debt markets.

In another post, we’ll build a fixed income portfolio that will be updated every month, consisting of mutual funds. We will add to them a small number of fixed income bonds that trade on the stock exchanges, for smaller portfolios (since they are illiquid). And we’ll have some real money behind these suggestions.

![]()

Disclaimer

Nothing in this newsletter is financial advice and should not be construed as such. Please do not take trading decisions based solely on the matter above; if you do, it is entirely at your own risk without any liability to Capital Mind. This is educational or informational matter only, and is provided as an opinion.

Disclosure: The authors at Capital Mind have positions in the market and some of them may support or contradict the material given above, or may involve a direction derived from independent analysis.

![]()

[/level-capmind-pro]