Most of us are fond of procrastination, especially when it comes to things that seem either too complex to bother for now or which the due time is still way off. Why bother now when it’s not yet time?

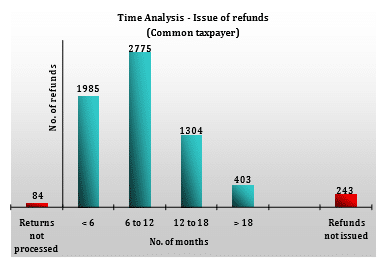

For years, one of the troubles with Income tax was getting refunds back in time. Before the Income tax department set up the Central Processing Cell at Bangalore, average time taken to process a refund was greater than 12 months. Here is a snapshot of how much time it took on an average prior to setting up of the cell (Data as per CAG sample)

A key reason for delays was the manual approach followed by the Income Tax department and lack of enough personnel with mounting volume of transactions. What started as compulsory exercise to efile returns for compulsory audit accounts has now been extended to all income tax payers. International evidence has shown that efiling provides for a faster processing than manual processing.

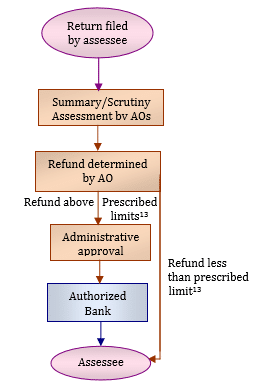

How does the Income Tax refund process take place?

Here is an interesting flow chart from the CAG report on the Income Tax Department.

With Income tax refunds having been streamlined enough to ensure that refunds happen within as short a time span as possible, the finance minister has now shifted to ensuing that the tax returns are filed on time to enable the whole process to be completed within the mandated time.

The current norms for late filing of Income tax returns were as follows:

If one has not furnished his return within the due date, he will have to pay interest on tax due. If the return is not filed up to the end of the assessment year, in addition to interest, a penalty of Rs. 5,000 shall be levied under section 271F.

Meaning: if the return isn’t filed by July 31/September 30, then you still have time till the next year’s March 31 to file returns. Only that you need to pay some interest on the tax, but if there’s no tax due, you’re okay. Only if you delay further than that, you’re fined Rs. 5,000.

In the current Budget the finance minister has gone one step ahead. The above penalty structure has now been slightly modified. If you don’t file the returns within the due date but does file within 31st December of the Assessment year, a fine of Rs.5,000 would be imposed. The fine doubles to Rs.10,000 for delay beyond that. If the filing is for income below Five Lakh, the maximum fine is limited to One thousand Rupees.

By this the government wishes to ensure that the process ends well before the New Year ends rather than it being a never ending process. This in turn will help in reconciliation of expected collection versus the actual collection.

And it means just one thing: if you value your money, don’t delay your filing. July 31st is for individuals who don’t need an audit. For those who do, the date is 30 September. The finance minister may have given you a bonus of Rs. 12,500 in the budget through a lower first slab, but don’t give away much of it by filing your return late.

Watch out: Budget2017 Fines You For Not Filing Tax Returns on Time

Like our content? Join Capitalmind Premium.

- Equity, fixed income, macro and personal finance research

- Model equity and fixed-income portfolios

- Exclusive apps, tutorials, and member community

Subscribe Now

Or start with a free-trial

Already a subscriber?

Login Now

Related Posts

India joins Global Bond Indexes: What it means and What it doesn’t

Indian bonds will soon be in global indexes, says JP Morgan. Looking beyond the rhetoric, we analyze what it really means. It's a nice party, but will this ...

Money’s getting expensive, and fast, and what you can do about it

The debt markets are cowering in fear. Short term rates are rising very very fast. And there's no respite even for the government. Here's a quick take one the ...

Podcast: Investing in a world with high interest rates

Deepak and Shray discuss on navigating the current investment landscape, what higher interest rates could mean for various asset classes, and the assets one ...