A lot of fund managers write letters, some of which like the one Buffett writes are widely anticipated & discussed threadbare once it’s out. The GMO Quarterly update while not having the following of Buffett still makes for a very good read.

The 1Q 2017 is out. One of the points he talks about is Asset Allocation and how the universally recognized 60 / 40 between Equity and Debt may still not help you sleep peacefully in the worst of times.

An investor holding a 60/40 S&P 500/Treasury bond portfolio in September 1929 would have had 39% of his money remaining by June of 1932. An investor holding 100% S&P Composite would have retained 18% of his money, and one leveraging his investment in the S&P 2:1 would have retained 1.8% of his money.

One of the greatest crashes ever recorded was during the Great Depression. As the above quote showcases, anyone who had leveraged just 1 time would have lost everything while one who had a simple 60:40 asset allocation between Equity and Debt would have still seen a drawdown in excess of 60%.

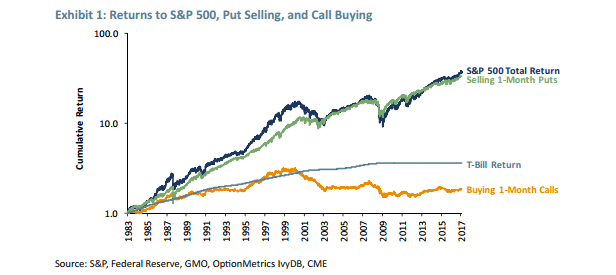

Put selling which is akin to being long is assumed to be a high risk strategy with limited upside. After all, you get all the downside and none of the upside other than keeping the premium. On the other hand, buying Calls means you get all the upside and none of the downside other than the cost of the option itself. So, what is a better strategy?

This chart is truly surprising as much as it’s enlightening. While the safe strategy of buying calls doesn’t even beat returns of T-Bills, the un-safe strategy of selling naked puts gets one a return pretty close to the Total Return of the Index.

In India, the talk in recent times is how the market has run ahead of valuations and is pricey compared to its historical averages. The same aspect has been said of the US Markets for a longtime using ShillerCAPE.

But what if the new valuations are not due to bubbly valuations but due to re-rating of stocks thanks to better fundamentals?

Compared to the pre-1997 era, the margins have risen by about 30%. This is a large and sustained change. And remember, it is double counting: above-average profit margins times above-average multiples will give you very much above-average price to book ratios or price to replacement cost. Counterintuitively, if we need to sell at replacement cost (most people’s view of fair value), then above-normal margins must be multiplied by a below-average P/E ratio and vice versa.

So, without further ado, the Report (GMO Quarterly). It’s worth your time.

What we are Reading: GMO Quarterly

Like our content? Join Capitalmind Premium.

- Equity, fixed income, macro and personal finance research

- Model equity and fixed-income portfolios

- Exclusive apps, tutorials, and member community

Subscribe Now

Or start with a free-trial

Already a subscriber?

Login Now

Related Posts

The Focused Way of Investing: Our Four-Quadrant Strategy and FY24 Review

FY24 brought us a 42% gain in our Capitalmind Focused portfolio, gently outperforming the Nifty's 29%. It's been a bit of a rollercoaster, especially these ...

CM Focused: Reducing our allocation to smallcaps & increasing cash

In the last few days, we have seen increased volatility in the mid and small-cap sectors due to regulatory actions, including restrictions on inflows into mid ...

Zudio: The Story Behind Trent’s Meteoric Rise

Trent, part of the Tata Group, is transforming Indian retail with unique store concepts, trendy products, and focusing on customer satisfaction. This article ...