What a come down it has been for Inflation. The number that we’re seeing is 2.19%, a very low headline for what has been one of India’s biggest worries in the past.  This is low and in fact, perhaps close to being too low.

This is low and in fact, perhaps close to being too low.

Remember: The Monetary Policy Commitee (includes the RBI) has a mandate to have inflation at 4% with a 2% buffer on either side. Meaning at the lower end it shouldn’t fall below 2%. It is at the border. Let’s look at components.

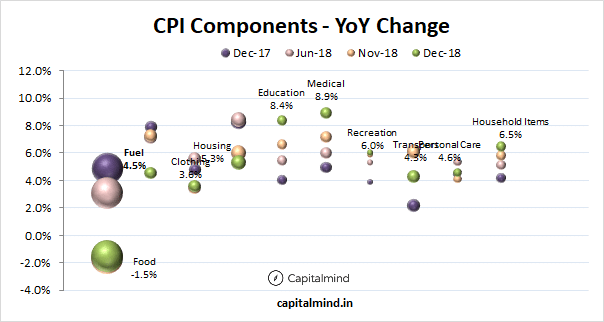

As you can see, the main issue is food inflation, which is now at -1.5%. This is a serious issue for the rural economy where income is primarily from agriculture, and thus there is serious rural distress.

As you can see, the main issue is food inflation, which is now at -1.5%. This is a serious issue for the rural economy where income is primarily from agriculture, and thus there is serious rural distress.

However, there may be some hope. The Index on Food started to fall around Jan 2018, which means from next month if food prices even stay stable, food inflation will go back up. This doesn’t mean the end of rural distress – it’s just optics because of the lower base.

What if you removed food and fuel? Those are traded items and they can go up and down fast. Inflation in other stuff (education, transport etc) can be more dangerous. So we look at core inflation instead:

As we can see: Core CPI is flat or so at below 6%. This will be a worry of sorts, because this has been climbing while food inflation fell.

Impact

The problem with inflation data is that no one really knows how the RBI or Monetary Policy Committee is looking at things. The RBI is trying to increase liquidity (a mini QE of sorts) even though there is no real liquidity challenge in the market (with huge amounts of reverse repo, the total liquidity borrowed from RBI is only 20,000 cr. or so. In challenging times, it would be over 100,000 cr. overnight)

But as we’ve seen in the west, the RBI’s pumping liquidity alone is not great. If you pump money into banks, there’s no guarantee they will cut rates or increase lending to the rest of the economy. (In fact, they won’t. Because now, their rates are linked to the repo rate through MCLR, and if the repo rates remain the same, they won’t cut rates)

There’s no data-bound reason to keep rates high except some fears that oh my goodness inflation will come back. But if it does, the RBI or the MPC can change track too. We believe that this data continues to provide enough scope for a rate cut, even if it’s a small one.